My Second-Biggest Financial Mistake

(This page may contain affiliate links and we may earn fees from qualifying purchases at no additional cost to you. See our Disclosure for more info.)

When I was married, waaay back in the day, I was working as a teacher in a suburb on the outskirts of Melbourne in the west. It wasn’t where I grew up, (I’m a Bayside girl from the other side of town), but it was where my husband had his business and love makes you do crazy things like move across the other side of the city to live. We delayed starting a family, so in the meantime, I discovered dog breeding and showing. Poppy and Jeff, in the photo below, are descendants of the dogs I bred at that time.

(This is one of my Christmas presents. My youngest son Evan21, took the photo and then blew it up – we now have a picture of the whole family. )

For 6 years dog breeding was my passion. I wanted to have a place where I could build proper kennels and give them space to run. My husband was a country boy and he wanted space around him, so we started looking for a block of land. We found one on the outskirts of Bacchus Marsh. 6 acres, already fenced. I can’t remember what the asking price was, but I know that we didn’t have the money upfront for a deposit. My husband used to spend everything he made…. but that’s a topic for another blog post. The only way we could come up with the money was if I cashed in my superannuation.

At that time I was about 27, I think. I had 30K in super that was ticking along quite nicely. In those days if you wanted to withdraw your super it was really easy, so that’s what we did.

Argh!!! I can’t believe I was that stupid! I had no idea of how compound interest worked, or of the importance of letting funds deposited while you’re young in an account like super being left to slowly compound and grow while time is on your side. Nup! We wanted that block so we took the money out. A classic case of short-term thinking.

While I was sitting here I just plugged the figures into a compound interest calculator. $30,000 for 30 years at 7% interest, with no further contributions being made. That $30,000 would have been worth $243,495 to me in another 4 years. Do you think that would make a difference to the when and how of my retirement plans if that tidy sum was added to my super? Do you think I’d still be working full-time, or would I have eased back to working 3 or 4 days a week if my super had an extra quarter of a million dollars?

That block in Bacchus Marsh cost me around a quarter of a million dollars.

Do you want to know the kicker? When I got pregnant with Tom25, we decided to sell the block and an investment property we had. My husband was suddenly nervous about servicing those debts on just one wage. Property values had fallen… we ended up selling the block at Bacchus Marsh for 30K LESS than we paid for it.

Yep.

At the time I was blissfully unaware of how costly those two decisions were. But now I know that if I’d understood the power of compounding, I would never have released the funds from my super. So I look now to my boys – those giants in the photo at the top of the page. I left the marriage when Tom25 was 5, Evan 21 was 11 months old and the other two were somewhere in between. I’ve raised them on my own and it’s up to me to teach them what I can about life, including their financial lives. If they can get their heads around compounding, they may be intelligent enough to not only avoid making the same mistake I did, but to actually turn it on its head and start actively harnessing that power.

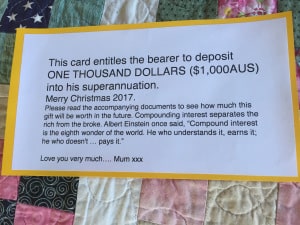

Earlier this year I sold our property and made a profit. I’ll discuss this at some stage later on on the blog. With Christmas coming up, and with the knowledge that I’d have not only my boys but also my nieces here, I decided to be a little theatrical and give them a gift with a string attached.

I handed out these ‘certificates’ at the end of when we were handing out the presents, when I had everyone’s attention. The accompanying documents were two tables I’d printed out from a compound interest calculator site. I wanted to make it crystal-clear what I was actually giving them.

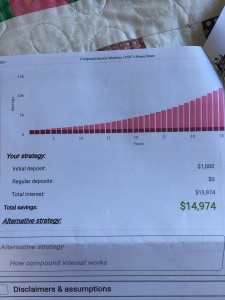

The first table shows what they’d end up with if they deposited the 1K and then never added another penny to it. I chose 40 years @7% interest (which is a conservative estimate for the interest rate. The Australian stock market averages just under 10% per annum.)

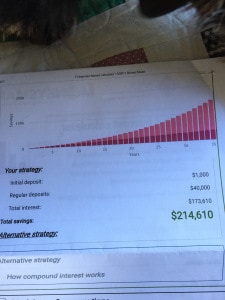

Now of course this table is totally unrealistic unless they choose to live off Centrelink benefits and never work a day in their lives. They’ll be adding to this amount every time they work and get paid. So I added another table – this time what would happen if they only seeded this account with another $1,000 each year.

Apart from Tom25, who’s an accountant and already has his head around this stuff, their minds were BLOWN. My nieces come from a family where money isn’t a topic of conversation and so they’re not exposed to these ideas at home. I was especially pleased that Jay18, my youngest niece, quietly came up to talk with me afterward, saying that she’d be interested in finding out more.

I also gave them all a copy of ‘The Richest Man in Babylon“. It’s a slim volume and I remember reading it when I was around their age and the lessons stuck. It’s up to them if they read it or not; I won’t be following up and nagging. I figure I’ll just present the information to them and they’ll access it when it becomes relevant to them.

The funny thing is, Tom25 said to me the next morning, “One of the books Dad’s been hassling me to read is ‘The Richest Man in Babylon’!” I laughed and said, “I’m not surprised. It’s a good book.”

I guess what this story proves is that even in the holidays, you can’t stop a teacher from teaching. I’ve put the information in front of all 6 of them and now it’s up to them how it percolates in their brains. It’ll be interesting to see how many of them, in a couple of decades or so, have taken the information and run with it. It’ll be my own little social experiment.?

Republished with permission from Burning Desire for Fire.