How Does the Debt Collection Process Work?

(This page may contain affiliate links and we may earn fees from qualifying purchases at no additional cost to you. See our Disclosure for more info.)

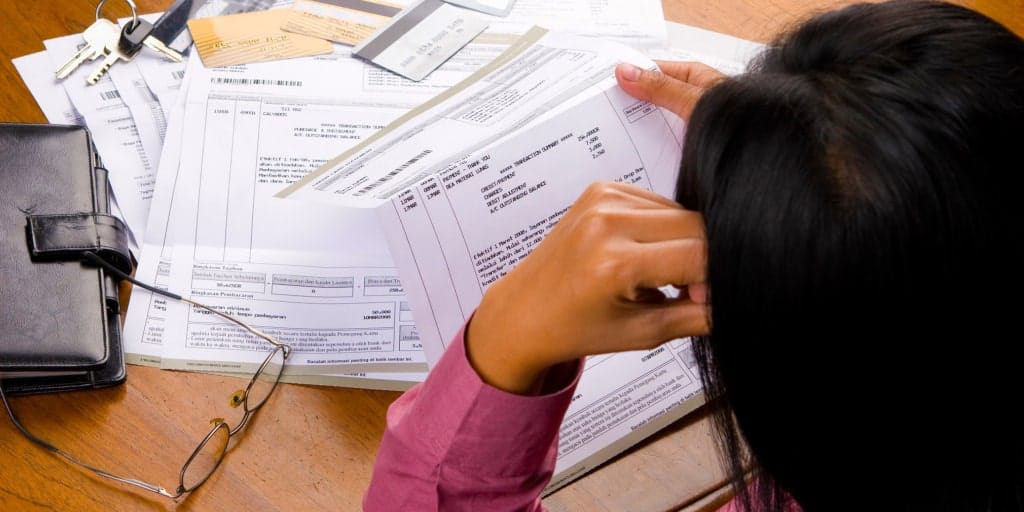

At some point in your life, you may fall on hard financial times and be unable to pay your bills.

Despite your struggles, your creditors still want to get paid. They'll likely employ a series of tactics called debt collection to get their money from you.

This process may involve constant (potentially harassing) communication from the debt collector as well as more severe financial consequences like a severely damaged credit score or a court judgment issued against you.

This is a tough spot to be in, but you’re not alone. According to Experian, more than 25% of Americans have accounts in collection.

But you can take steps to educate yourself and become familiar with your rights, learn how to handle the situation effectively, and discover how to shore up your finances to prevent this from happening again.

Let’s get started.

What Debts Can Be Collected?

While any debt can go into collection, for the most part, unsecured debt such as credit cards, medical bills, or student loans are the typical targets of debt collection.

Secured debt, like car loans and mortgages, offers the creditors collateral they can repossess in place of going through a drawn-out collection process.

Who Collects the Debt?

Initially, the original creditor will attempt to collect on past due accounts. Ultimately, they may sell the debt to a third-party debt collector. Third-party debt collectors may be from a debt collection agency or a law office.

The Debt Collection Process

Debt collection is a long process, and events happen in stages. On one hand, the slow-moving proceedings prolong the pain of the situation. On the other, it gives you ample opportunity to respond and try to fix the issue.

Here are some general events that you can expect:

- When you first miss a payment

- Creditor will cordially and repeatedly remind you to pay

- You may incur late fees

- When you are 30-60 days past due

- Creditor will continue to contact you and communication will become less friendly

- Creditor will report the delinquency to the credit bureaus

- After 60 days late, you may be charged a penalty rate (higher interest rate) on your credit card accounts

- Several months past due

- Creditor may sell the debt to a third-party debt collector to ensure they receive some payment

- Each payment missed will be reported to the credit bureaus

- After 180 days (6 months) past due, credit card accounts will be charged-off and closed (which means you can no longer bring the account to current)

- Eventually

- Creditor or third-party debt collector may try to sue you which could lead to wage garnishment, bank levies, or property liens

How to Respond to Debt Collection

Depending on your circumstances, there are different actions you can take to prevent collection efforts from taking root or improve the situation at hand.

The most important takeaway is that ignoring the problem will not make it go away — it will actually make it escalate.

- When you start to struggle financially – Contact your creditors as soon as possible

- When you're contacted by a debt collector – Determine if you legitimately owe the debt

- If you don't owe the debt – Contest it

- If you do owe the debt – Try to arrange a payment plan

- Should you get sued – Respond to the summons promptly

Let’s explore each in further detail.

Contact Your Creditors ASAP

As soon as you realize you can’t afford to pay your bills, contact your creditors — before you miss a payment.

They may be able to work with you and provide an alternate payment plan to avoid late fees, interest rate hikes, or hits to your credit report – sparing you from the long and arduous debt collection process outlined above.

Determine if You Owe the Debt

If a debt collector contacts you for payment, you should verify the debt is legitimately yours before doing anything else.

If you speak with them over the phone, ask them to send you detailed information about the debt in writing.

When reviewing their documentation, check the original creditor, the date the debt was incurred, and the balance due against your records, including your credit report.

Contest the Debt

If you personally did not incur this debt or have already paid it off, you must dispute the debt in writing within 30 days of receiving the information about it.

The Consumer Financial Protection Bureau (CFPB) provides sample letters you can send to the debt collector. They must, in turn, respond with written verification of the debt within 30 days of receiving your notice to contest it.

Also, they must not pursue further collection activities until they provide said verification.

Pro Tip: Keep copies of all correspondence you send and receive regarding this debt.

More information about contesting a debt.

Arrange a Payment Plan

If you know you truly owe the debt, it’s wise to see what payment plans the debt collector will offer.

You may be able to pay a fraction of your original balance, stop the collection calls, and avoid getting sued. However, even if they present you with an enticing deal, proceed with caution.

Be sure you can actually afford the payments (no sense in going further into the hole) and get the plan details in writing before forking over a single cent.

Alternatively, if you don’t want to negotiate repayment terms alone, you could pursue credit counseling or debt settlement services. Each has its own rules, advantages, and pitfalls, and should be researched carefully before taking any action.

And remember, regardless of which method you choose, the debt collector does not have to provide a payment plan or settle for less than the full balance due.

If that’s the case, you’ll need to save up until you can pay the debt off in full, knowing that collection efforts will continue.

Related reading: Should you declare bankruptcy?

Respond to Any Summons Promptly

If a debt collector attempts to sue, you must respond by the deadline listed in the summons.

Failing to respond will likely result in the court assuming the debt is valid and issuing a judgment against you.

To satisfy the judgment, your wages may be garnished, your bank accounts may be levied, or your property may have a lien put on it.

Court decisions are difficult to reverse, so it’s in your best interest to fight in court — or attempt to negotiate with the debt collector before the hearing.

Pro Tip: If faced with a lawsuit, it may be worth consulting with an attorney — especially if the debt is old or if you believe the debt collector has violated any of your rights described below.

Understand Your Rights During Debt Collection

The Fair Debt Collection Practices Act (FDCPA)

While the debt collection process can be stressful and overwhelming, remember: you have rights.

The Fair Debt Collection Practices Act (FDCPA) governs what third-party debt collectors can do in pursuit of getting their money, and prohibits them from acting in an abusive or deceptive manner.

As per some of the significant provisions of the law, debt collectors must:

- Tell you that you have the right to contest the debt

- Not contact you before 8 am or after 9 pm in your local timezone

- Respect your inability to take personal calls at work and refrain from calling you there

- Go through your attorney if you’ve instructed them to do so

- Not tell other people about your debt (but may call friends, relatives, or your employer in an attempt to get your contact information)

- Honor your written wishes to stop contacting you (but may confirm receipt of your request and state that further collection efforts such as a lawsuit could still occur)

Please note that the FDCPA typically does not apply to the original creditor.

However, each state has its own legislation about debt collection practices that may cover them. Check with your state’s attorney general to learn more.

To get more details about the FDCPA, or to file a complaint with the CFPB.

Statute of Limitations

Although it may seem like it, debt collectors can’t hunt you down forever.

The statute of limitations, which varies from state to state and debt type, dictates when the debt collector no longer has a legal right to sue you.

It’s important to note, however, that they may still contact you in an attempt to collect the debt. After all, the obligation never truly disappears.

Caution: If you make a payment, you could restart the clock and lose the protections of the statute. Check your state’s laws and whether your original credit agreement specifies which state’s laws would be applicable so that you can be sure of your rights.

Long-Term Ramifications of Debt Collection

The debt collection process can literally drag on for years.

That’s a long time to deal with the stress of constant, possibly threatening communication from debt collectors, always worrying if you’re going to land in court.

That burden can take a heavy toll on your mental and physical health.

And, if you do end up with a judgment against you, it could make a difficult financial situation even more dire for your household.

Plus, accounts in collection will linger on your credit report for seven years from the date first reported as delinquent.

This ding to your credit score can cause a whole host of problems such as not being able to access additional credit when you need it or disqualifying you from certain types of employment.

The good news? The impact of the delinquent account on your credit score lessens over time — even before it entirely falls off of your credit report.

Recovering From or Preventing Debt Collection

As you can see, debt collection is no joke.

At best, it will mar your credit history. At worst, it could ultimately make your family’s budget impossibly tight and be detrimental to your well-being.

So how can you recover from it — or prevent it from happening?

Implement these financial best practices:

- Assess your financial habits and situation:

- Do you spend more than you earn?

- Do you often misplace bills?

- Have you been hit with an unexpected, unfortunate set of circumstances (ex. high medical bill)?

- Make a plan to address any shortcomings:

- Establish an emergency fund.

- Create (and stick to) a budget.

- Organize your bill pay process by setting up payment reminders or autopay.

- Track and monitor your spending, assets, and liabilities.

- Eliminate your debt:

- Trim down your budget

- Find ways to earn extra cash

- Pay off your burden – They can’t collect what you don’t owe!

- Avoid new debt: As you’re getting back on your feet or establishing a solid financial foundation, try to refrain from taking on more debt. As they say — stop the bleeding!

Final Thoughts on Debt Collection

Dealing with debt collection is an anxiety-provoking experience that can have dire, long-lasting financial consequences.

However, you have rights and options, that if leveraged correctly, can make the situation much more bearable.

While this article gives a good overview of how debt collection works, every situation is different, and laws can change.

We encourage you to seek professional financial and legal guidance to ensure the best possible outcome.

Article written by Laura