Why Gen X Women are anxious about their finances

(This page may contain affiliate links and we may earn fees from qualifying purchases at no additional cost to you. See our Disclosure for more info.)

It's 2020; old age is looming closer, accompanied by the threat of a lackluster retirement.

Of course, you're anxious about your financial future.

But you're too busy taking care of everyone else to do anything about it.

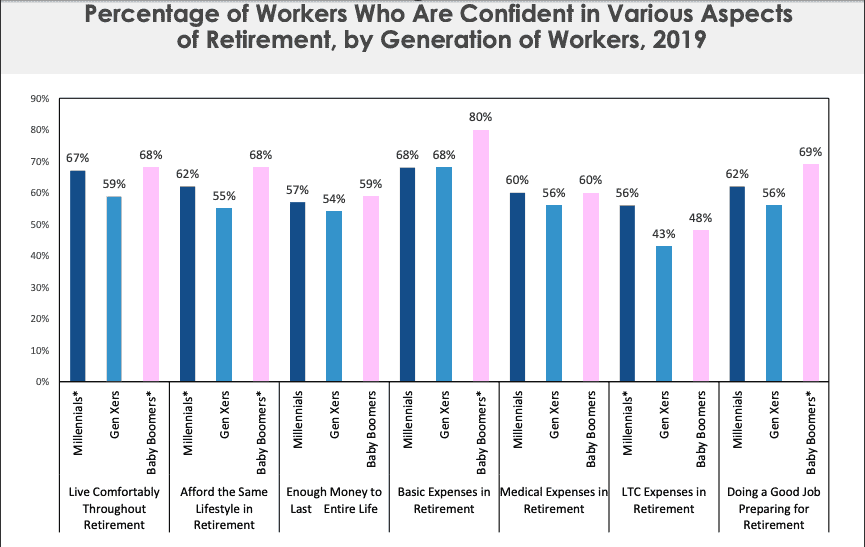

According to this study by Employee Benefit Research Institute, members of Generation X feel less confident about retirement than millennials and baby boomers.

Over half of Gen-Xers don't think their current financial reality will allow them to:

- live comfortably throughout retirement;

- afford the same lifestyle in retirement

- have enough money to last their entire life;

- cover basic expenses in retirement

Albeit quite an unsettling reality, things aren't hopeless.

Sure, life has been an uphill battle for today's middle-aged women, but that doesn't mean you have to accept defeat.

When seizing your financial power, you will have to mentally and financially overcome a few obstacles. But not without first identifying them.

Here are some reasons Gen X women don't feel confident about their financial futures:

Gen X Women Have Fewer Retirement Options

A little history

The height of second-wave feminism in the early 1960s set the financial tone for Gen X women today.

As an expansion of the first feminist movement, it called for gender equality in the workplace and legal equality.

Women wanted to be in control of their financial futures, and they weren't taking “no” as an answer.

As a result, Gen X women — who were born around that time — stepped into a drastically improved economic reality.

However, the financial literacy gap between men and women still hadn't changed.

Women were now able to work and earn relative financial freedom but had little to no knowledge of what to do with their money.

Fast-forwarding to the present

Consequently, Gen X women are less educated about retirement issues than both boomers and millennials, with 67% feeling their financial planning and savings are not on track for retirement.

Furthermore, “the cost of a college education was higher for Generation X, and the jobs were more scarce,” according to Gen X aficionado Jennifer McCollum.

That fact, paired with the well-known gender pay gap, provides context for the lack of financial preparation amongst Gen X women.

Today's middle-aged workers are also responsible for their retirement in a way their parents were not.

Traditional (defined benefit) DB pensions provide workers with guaranteed lifetime retirement and benefits reflective of their earnings near the end of their careers.

Unfortunately, employers are increasingly opting for defined contribution (DC) pensions, which require workers to fork over more cash if they want a healthy retirement plan.

Gen X Women Face More Financial Responsibility and a Shifting Work Landscape

Gen X women are caretakers for the much larger generation of boomers and the similarly populous millennial generation.

This causes a unique financial strain, affecting long-term plans for career, retirement, savings, insurance, etc.

It also doesn't help younger boomers who have seniority and older millennials are squeezing Gen X women out of the workplace.

As generation expert Hannah Ubl puts it, Gen-Xers feel “frustrated, as millennials are nipping at their heels and have nowhere to go.”

The startup revolution is causing a bit of unrest for middle-aged workers as well.

While Generation X spear-headed this movement, society is quickly replacing them as the “entrepreneurial generation.”

This shift is partly because Gen-Xers embraced entrepreneurship to express their cynicism towards corporate careers.

Meanwhile, millennials are genuinely optimistic about their work, solidifying themselves as the “purpose over paycheck” generation. The source of motivation is different.

As a result, companies are forcing Gen X out, and the face of entrepreneurship is quickly changing to account for millennial work trends like:

- gig economy/wide-scale freelancing

- remote work

- tech-based jobs

- decreased in manual labor

Sexism, Paired with Worsening Ageism, Pushes Gen X Women out of the Workplace

In addition to being slightly hurtful, the moniker “forgotten generation” also allows for rampant ageism and sexism amongst Gen X workers.

Amy Tobin of ArCompany recounts being “cautioned by superiors about hiring anyone over 40, as they are in a protected class and more difficult to fire.”

It's not rare for middle-aged workers to be intensely aware of unfair treatment embedded in their ageist work environment.

Many Gen X women have even sued former employers for overt age discrimination.

Some common examples include:

- Demotions and younger aged superiors

- Requiring a higher standard of performance from older workers than their younger coworkers

- Exposing them to work-based humiliation and an unpleasant work environment

Although these lawsuit cases were successful for the victims, women were still ultimately forced out of the workplace because of their age.

No amount of money can change the way that makes a person feel.

Even worse, ageism often exacerbates the sexism\most women experience throughout their careers.

At least 18% of Gen X women have encountered gender bias at work, reports this study.”

How Can Gen X Women Cultivate Financial Empowerment?

Financial empowerment is the secret to a joyful and stress-free life. It doesn't mean you're rich or have more money than you can ever spend.

Instead, it's an indication that you're in control of your finances and have a cemented plan for your future.

When you're looking to cultivate financial empowerment for yourself, implement the following money practices today.

Related: 11 Ways to Increase Self Confidence

Prioritize Your Savings

Admittedly, Gen X women have not had the financial luck of the draw. However, there's a noticeable contrast in the saving habits of your generation vs. those of millennials.

As the caretakers of baby boomer parents and millennial children, you haven't had the chance to think about your financial well-being, let alone put money toward securing your future.

Although the average caregiver is a middle-aged woman, “[today's] women are too busy to even think about focusing on themselves at 40 and 50.”, says AARP national family and caregiving expert Amy Goyer.

With middle-aged workers shouldering most of their retirement responsibility, having money saved away can be the difference between an unclear financial future and a fully mapped-out retirement plan.

Take Control of Your Financial Education

As mentioned above, Gen X women struggle with financial literacy more than their male counterparts, millennials, and baby boomers.

You can successfully calm anxiety about your financial future by learning what to do with your money.

Two areas of financial literacy you should delve into today are money management and retirement.

Money management

You've worked your butt off to obtain an adequate salary, and now you need to learn how to manage it responsibly.

Consider taking the time to perfect these skills:

Retirement

This is the big'un. Much of the concern surrounding your financial future stems from not knowing what life looks like after retirement.

Having a retirement plan will provide clarity for what life looks like 5-20 years from now.

By the age of 50, you should already know:

- What your retirement number is

- Where your retirement income is coming from

- Where you'll live during retirement

- Who you'll still be responsible for caretaking

- How will your caretaking be handled, if necessary

- Which retirement plan and savings goal will work for you

Know What Age Discrimination Looks Like (And How To Fight It)

In a push to protect older workers, The Employment Act (ADEA) was enacted in 1967, prohibiting workplace age-based discrimination and harassment.

Regardless, age discrimination continues to affect many workers aged over 40 and can result in:

- hiring bias

- explicable layoffs and firing

- pay inequality

- unfair job assignments and promotions

- benefits that decrease with age

Although ageism is common in the workplace, remember your work, experience, presence, and role is valuable.

When you have the opportunity, speak up and correct coworkers who make discriminatory assumptions.

Younger workers and superiors often imply that their older peers are:

- Incapable of using technology

- Too tired to work hard

- Inflexible/Lack agility

However, you know your limits and capabilities.

You vastly increase your chances of overcoming age-based inequality if you know your rights and are adamant about enforcing them.

Always demand to be treated with the respect and dignity to which you are legally entitled!

Get Life Insurance. Now.

You won't have to worry about what your kids will do when you're gone if you secure financial options for them upon your passing.

Yes, a life insurance policy will increase your monthly expenses, but it's well worth it.

Once sure that your inevitable passing away won't be financially devastating, you’ll remove the guilt of focusing on yourself.

What Does This All Mean?

You've been fighting for your financial future all your life. It hasn't been easy, and as a matter of fact, you've faced just about every obstacle possible.

You're the sole caretaker of your children and possibly your aging parents.

You have far fewer retirement options than previous generations.

Your career is always vulnerable to the ravages of sexist ageism.

It's no wonder your finances aren't up to par — heck, you're tired!

But now that you've come face to face with what’s really preventing financial empowerment buckle down and do the work for the future you deserve.

Next:

- How Do I Build My Financial House For A Financially Secure Future?

- Retirement 101: Kick Your Retirement Planning Off Right [Book Review]

Article written by Lyric