Can I Invest with Five Dollars (or less)?

(This page may contain affiliate links and we may earn fees from qualifying purchases at no additional cost to you. See our Disclosure for more info.)

Have you been wanting to invest but you don’t know where to start?

Do you think investing is too complicated or too risky?

Are you one of the millions of Americans who can’t even fathom how you’d come up with extra money for investing?

Micro-investing could be the solution for all of these questions.

Micro-investing is tailor-made for the beginning investor of modest means. It allows you to easily invest very small amounts of money in stocks that will grow in value, pay dividends, and earn compound interest over time.

“Small amounts of money” is not an exaggeration. It could be $1.50, seventy-five cents, or even a quarter.

When you see how your extra change transforms over time, you’ll be motivated to learn more, invest more, and make serious headway on your financial goals.

It all starts with that first investment.

How Do I Start?

Micro-investing is done through an app. You’ll need to do some research to find the one that’s right for you.

Several reputable websites like The Balance, Nerd Wallet, and Investopedia compare the major ones, examining aspects like cost per trade, ease of use, and availability of educational resources.

You’ll certainly see several mentions of the big names in micro-investing like Acorns and Stash, but give the newer apps a chance, too. (Competitors might be offering a great deal!)

While you have several choices, structurally these apps are all the same. They are simply a portal you use to put your money into the market.

Create a Micro-Investing Account

Once you’ve picked an app, you’ll create an account and link it to your bank. You must do this to use the app; direct bank transfers are the only way to fund your account.

If this leaves you feeling a bit apprehensive, then take some extra time to review the company and learn more about its security measures.

Because the company will need to verify all of your documentation (photo ID, social security number, physical address, etc.) it will take a few business days before your account is active.

Investor Profile

Once your account is set up, you’ll create an investor profile. You’ll be asked a series of questions, all designed to determine your risk tolerance.

Are you willing to invest in very volatile stocks for the opportunity to make incredible gains? Or would you rather invest in low-risk stocks for lower but dependable earnings?

Maybe, like most folks, you’re somewhere in the middle.

You’ll be able to clarify your position based on the app’s scale.

It will usually provide risk categories like: very low, moderately low, moderate, moderately aggressive, and aggressive. You just need to pinpoint where you fall on the scale.

What am I Investing In?

Most micro-investing platforms invest your money into exchange-traded funds or ETFs. Unfamiliar with ETFs? Here’s a quick primer or see this article for more details:

- An ETF is a fund made up of several different stocks. It’s a very diversified mix, containing companies of different sizes across different sectors. Think of it as a big vat of soup.

- Buying a share of an ETF is like taking a small bowl of soup from the vat. You have all of the ingredients, they’re just scaled down proportionally.

- When the fund makes money, you make money in proportion to the size of your investment.

Your risk profile dictates the kind of ETF you’ll be invested in.

If you’re able to tolerate risk, your money will go into an ETF that includes high-risk securities. When you’re risk-averse, the app will direct you to an ETF containing low-risk securities.

There’s an ETF for most every investing style, so you can be sure that you’ll be matched appropriately.

Start Micro-Investing!

There are two ways to invest through your app: direct funding or round-ups.

Direct funding:

You tell the app exactly how much money to invest.

If you have unpredictable income and you’re not sure when you’ll have extra money, you can wait until you’re ready and then make a one-time transfer. ($5.00 is usually the smallest amount that you can contribute.)

If you have dependable income and you want to make regular contributions, you can set up your account to invest on a schedule.

It might be $5 per week, $25 a month, or some other amount. You can easily increase or decrease the amounts and frequency at any time.

You could even take part in a 52-week savings challenge and increase the amount invested each week.

Round-ups:

This is an INGENIOUS way to invest. Set the app to round up every purchase that posts to your bank account. If a charge comes in for $3.60, the app will round that up to the next dollar and apply .40 to your investment account.

It does this for each and every charge, meaning you could invest anywhere from a few dollars to twenty or thirty dollars a month, depending on how many charges go through your bank account.

If you like the effect that round-ups have on your account (and you will–they add up fast!) then you can connect your credit and debit cards to the app, too.

That way, every single transaction you make will be part of the “round up and invest” machine.

Want to super-size those investments? You can set your app to do a double round-up on all of your transactions.

The $4.23 that you spent at the coffee shop means you’ve invested $1.54. (Seventy-seven cents on the round-up times two.)

Most apps have a “multiplier” option that you can use to super-size your round-ups to your preferred amount.

You can also use a combination of direct funding and round-ups. Many folks make regular weekly or monthly contributions to the account in addition to keeping their round-up investments rolling in.

You may also want to make one-time investments when you come across an unexpected windfall (like a bonus or a tax refund). Using this multi-pronged approach makes your fund grow even faster.

How Much Money are We Talking About?

Excellent question. It’s important to keep your expectations in check. After all, it’s called “micro” investing for a reason.

You can’t expect small investments to yield huge results in a short amount of time. But you CAN expect a good return on your investment with several years in the market and regular funding of the account.

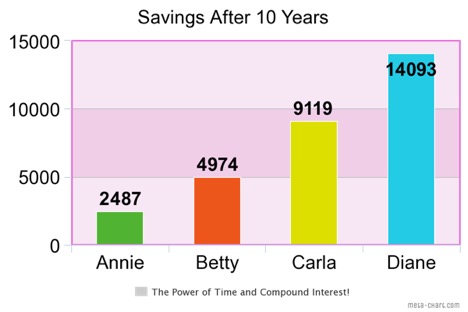

Here are some sample investors to consider:

Annie

Uses round-ups attached to her checking account for an average of $15 per month.

Betty

Uses 2x round-ups attached to her checking account for an average of $30 per month.

Carla

Uses round-ups attached to her checking account and credit cards for an average of $30 per month. Also invests $25 monthly for a total investment of $55 per month.

Diane

Uses 2x round-ups attached to her checking account and credit cards for an average of $60 per month. Also invests $25 monthly for a total investment of $85 per month.

Assume that all accounts stay invested for ten years and earn an average 7% return. Here’s how they compare:

Now, these amounts aren’t going to change your overall financial picture. Not drastically, anyway. But remember–this is money you can amass by doing almost NOTHING.

This is spare change you’ll never even miss. You could even go so far as to say it’s money you would have otherwise frittered away.

When you put it into perspective, the sample micro-investing accounts do very well for themselves!

Earnings = Taxes

Micro-investing puts your money into a REAL investment account.

Withdrawing funds subjects you to taxes on your earnings, interest, and dividends.

Anything tax-related can sound scary, but don’t let it keep you from investing.

You’re looking to create an investment that will grow with compound interest over time–right?

So appreciate the restrictions on withdrawals for what they are–a safeguard that ensures you’ll leave your money alone to grow.

If you do need to take out the money, you’ll be subjected to capital gains taxes on your earnings.

The rate will depend if the money was in the account for under a year (a short-term gain taxed at your regular income rate) or for more than a year (a long-term gain taxed between 0 and 15%).

Savings GOALS!

Money management works best when you have a specific financial goal in mind.

Try to attach an end goal to your account so you can really feel what your money is supporting each time you make a contribution or check your balance.

Some investors save for a:

- Wedding

- College Education

- New Home

- A Big-ass Trip After Retirement (or any other big-ass trip)

Final Thoughts on Micro-Investing

Managing money is work. It takes knowledge, planning, and discipline to create a savings plan that aligns with your budget and your risk tolerance.

Opening a micro-investing account is an easy way to get off the shore and test the waters of investing without having to put a lot of your hard-earned money on the line.

Although a micro-investing account isn’t a cure-all that will provide you with major lifestyle changes, it CAN be a great way to meet a specific financial goal and learn more about the power of investing in the process.

Be sure you understand the risks (no investment is fool-proof), the obligations (you’ll owe taxes at some point), and the rewards (the magic of compound interest!) and consider adding this strategy to your financial planning.

Article written by:

Guest contributor, Kathy G. Mills, founder of the website Wall Street is Waiting. She is also the author of the award-winning book Market Mojo: A Beginner’s Guide to the Stock Market. As a Certified Financial Education Instructor (CFEI) Kathy leads investing seminars that “take the fear out of finance” and help participants plan for their financial future. Follow her on Twitter @WallStreetWaits