Sharing Expenses as a Couple: Making it fair

(This page may contain affiliate links and we may earn fees from qualifying purchases at no additional cost to you. See our Disclosure for more info.)

You’ve decided it’s time to move in together. It’s a big step in your relationship, and you’re excited about the future.

You’ll have to each decide which of your belongings you can share in your new place.

Another thing you’ll have to figure out? How to share expenses when living together.

The best way to split expenses when you live with your partner – is the way that works for both of you.

We'll take a look at 6 different options below and some personal and financial considerations to help you decide.

Choosing whose couch or dishes to use might not be too difficult. But deciding how to divide up your living costs can be a more significant challenge.

One of you might want to split each bill equally, and the other wants to use a percentage of your income to figure out what you pay.

Each person paying specific bills is another option. Some couples prefer to pool all of their money together.

The great thing is, there’s no right or wrong way.

Make Your Plan Early

Once the initial excitement of moving in together fades, reality sets in. You’ll go to work, get groceries, do laundry and vacuum, go out with friends, and pay bills – just like you did when you lived apart.

You like to get your car washed each week and have no interest in cutting cable TV. Your partner prefers the AC on all the time and could care less about turning lights off when leaving a room.

While none of these were issues before moving in together, they can indeed become a source of tension when you have joint finances.

Before you decide how to share expenses, consider different options. If you believe putting money together is a vital sign of commitment, ask yourself why.

If you have a smaller income or more debt than your partner, how will splitting expenses 50-50 make you feel?

You can be in love and still disagree about how you should budget and spend money.

While you can certainly change how you’re sharing expenses if your plan isn’t working, being proactive and talking about it before moving in together can help prevent issues in the first place.

Remember, research shows the more a couple argues over money, the more likely they are to split up over money. Rose-colored glasses rarely save a relationship when people can’t communicate about their finances.

Paying For Household Expenses You Share

Before you read about different ways couples can share expenses, realize that there are many variables – both personal and financial – to consider.

- Are you moving into a home one of you already rent or own?

- How much debt do you each have?

- Is there a significant discrepancy in your incomes?

- Are children involved?

- Are there financial obligations to former spouses?

- Is one of you a spender while the other is quite frugal?

All of this matters when you move in together and need to pay bills.

It’s important to note here that shared household expenses are your focus at this point.

While a couple can determine which expenses they’ll share – rent*, utilities, and food is where most start.

We suggest (especially early on) that each person continues to pay their own debts (i.e., credit card balances, car loans, student loans.) And avoid cosigning loans for one another.

*Note: If you buy a house together, you’ll share the mortgage, taxes, insurance, and cost of major repairs instead of rent. If one of you owns the home before moving in together, there is more to consider.

Whether the other partner pays half of the mortgage, pays “rent” to the person who owns, or makes some other arrangement – consider the legal and long-term impact of this decision for both of you.

While your payment arrangement might make sense now, don’t forget to protect your future self too.

6 Options for Sharing Living Expenses

Review and discuss these six options with your partner to find one you're both comfortable with adopting.

1) Share Household Expenses Equally

If you lived with roommates in the past, you probably split expenses equally. So it may make sense to continue this with your significant other.

Because you’re more than just roommates now, you might add in other joint expenses such as entertainment or vacations.

When each of you contributes equally to the household, you may have fewer issues. But you could run into problems if your income or debt levels are very different.

To pay shared expenses, you might open a joint checking account and contribute a set amount each month.

Then you can set up a “budget date” to review monthly spending. This transparency helps build communication around money and will allow you time to talk about both short-term and future financial goals.

One person can also pay all of the bills and be reimbursed half by their partner. If you decide to do this, make sure you still set up regular money meetings to discuss joint finances and shared goals.

Considerations:

- If one partner has plenty of disposable income, while the other is hustling hard to pay off loans or credit card debt – there could be hurt or negative emotions, a perceived imbalance of power, or a mismatch of goals. Unresolved these feelings can turn into significant issues.

- While it isn’t something you want to think about, sharing expenses equally also might make it easier in the event you break up.

2) Share By a Percentage of Gross Income

Many people see sharing expenses as a percentage of gross income as the most equitable way to pay joint bills when you’re living together. This is the “fair but not equal” scenario.

To determine the percentage to pay, it’s suggested you add your gross incomes together and then divide the higher income by the total and multiply by 100 to get the percent.

That becomes the higher earners' contribution.

Subtract that percentage from 100 to get the percentage the lower earner should contribute to joint bills.

$65,000 + $38,000 = $103,000

$65,000/ $103,000 = .63 x 100 = 63% is what the higher earner pays

100% – 63% = 37% is what the lower earner pays

Considerations:

- One thing to think through and discuss is whether paying extra will cause the person who pays more to end up resenting this decision, which could eventually harm your relationship. If that’s something you could see happening, you might reconsider moving in with the person now.

- While one person may earn more, they may also have more debt or other responsibilities. Thus, this scenario might not be so fair, after all.

3) Share Housing By Percentages and Other Expenses Equally

“Fairer but still not equal” might be a good way to describe this option.

Sharing significant expenses like rent by a percentage of gross income described above allows the lower-earning member of the couple more money to put toward other debt or financial goals.

Contributing equally to the other shared expenses like utilities and food, still allows the lower earner to feel they are “pulling their weight” for at least part of household spending.

4) Divide Up the Specific Bills and Pay Them

You and your partner may decide to look at all of your household expenses and each assume “ownership” of paying specific bills from your individual accounts.

This can be a relatively quick and easy way to share without needing a joint bank account.

Remember, quick and easy still needs to be monitored.

Consideration:

- If one person pays a sizeable fixed expense (mortgage or rent) while the other picks up bills like electric, gas, internet, and food – make sure any variations in those bills aren’t putting an unequal burden on that person.

5) Combine and Conquer

Some couples who move in together, decide to join their financial lives too, especially once they consider marriage.

They create a bank account in both names and both deposit their paychecks into it. They usually pay all bills from it – no matter who they belong to.

This can be an easy solution and the one that supports your long-term goals as a couple. But it can also create issues if the relationship doesn’t work out.

Consider what you could lose if you broke up and talk with your significant other about how you would protect each other.

If marriage is a part of your future, create a financial mission statement together, and consider a prenuptial agreement.

It may be an awkward conversation, but if you care about and love each other, you need to be able to discuss challenging topics like this.

6) Combine Plus

This option works for many partners who want to combine finances once they are committed to each other for the long run, but also want to maintain their own accounts for personal spending.

In this situation, the couple budgets an equal spending allowance, which is transferred from the primary joint account to each partner's personal account.

This allows individuals to spend money on experiences, personal hobbies, or gifts important to them.

The crucial thing here is to agree on the allowance each can spend freely, without needing to agree on how the money is spent.

Tracking Made Easy

Once you determine which up the above methods you'll use, you will also want to consider how to best track your expenses together.

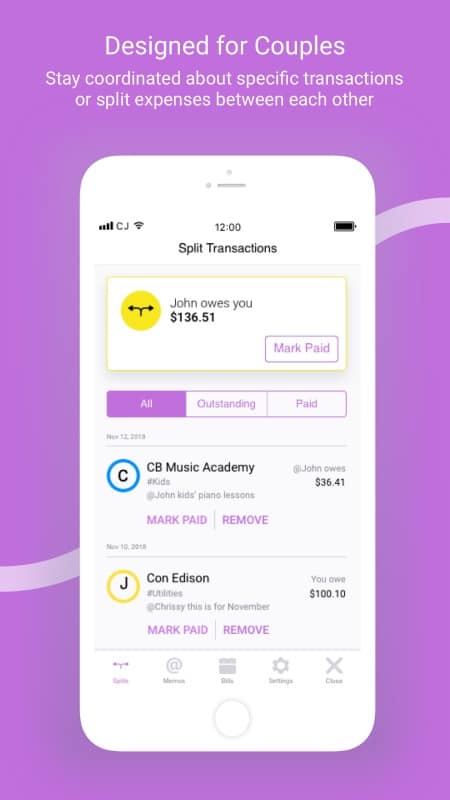

We recently learned of Zeta, a mobile and web app helping couples track and share their finances together – with 100% control over what you do or don't want to share!

The Zeta app allows you to manage your individual and shared monthly spending.

You can split transactions, share your financial picture with your partner, track your overall net worth, review your monthly spending, and get better at managing money together – on your own terms.

Other Financial Considerations When Living Together

As mentioned above, both your individual life circumstances and your life as a couple will determine what works best for you in terms of sharing expenses.

Some partners have little trouble finding a good way to manage their financial lives together, and others quickly learn that splitting up the bills isn’t so easy to do.

Starting slow and sticking to just sharing expenses – from a joint account or not – is one way to stay in control of your own finances.

Moving in with someone doesn’t mean you have to share everything – including their debt.

If over time you feel you are ready to commit to a full joint financial relationship, you can always take that step. But it’s hard to put it in reverse and ask for your money back.

Whether you decide to have a formal agreement or not for your expenses, you should also think about an “exit” plan for your living situation.

While it’s not the most romantic thing to discuss, it's important you do.

- If you can’t live together for some reason – who will stay in the apartment or house?

- If your significant other moves out, can you cover all of the monthly expenses alone?

Don’t forget to review your plan to share living expenses whenever you have a life change too.

- A different job or employee benefits package might change how you divide things up.

- If you move, have a significant illness, or have a child – you may need to reconsider how each of you contributes to the cost of running your household.

As you spend more time living together, you’ll learn a lot about each other. Some of your money beliefs and behaviors may align perfectly but don’t be surprised if some don’t.

Your upbringing, values, experiences, and life decisions made up to this point in time all affect your money life. Unless you see some serious red flags, keep communicating, learning about each other, and moving forward.

Written by Women Who Money Cofounders Vicki Cook and Amy Blacklock.

Amy and Vicki are the coauthors of Estate Planning 101, From Avoiding Probate and Assessing Assets to Establishing Directives and Understanding Taxes, Your Essential Primer to Estate Planning, from Adams Media.