How Do I Teach My Teenager About Money?

(This page may contain affiliate links and we may earn fees from qualifying purchases at no additional cost to you. See our Disclosure for more info.)

One of the most important jobs we have as parents is to teach our children how to navigate the adult world.

An important skill they’ll need to master is managing their money.

Starting while they're young is a good plan, but if you've missed that boat, it's not too late.

So how can we successfully teach our kids to manage money when they’re teenagers, still living at home, and dependent upon us for most of their monetary needs?

Some school districts, realizing the importance of educating young people about money, have begun offering personal finance classes in high school.

North Carolina recently became the twentieth state to require high schoolers to complete a course in economics and personal finance to graduate.

Topics taught to teens include paying for college, using credit cards, and taking out a home mortgage.

Even if your state doesn’t require such a course in high school, however, there are ways you can teach your teenager how to manage their finances.

Related: Setting Up Your Financial Life After College

Teaching Your Teen About Money

Here are six essential money topics and tools to discuss and use with your teen to boost their financial literacy.

- Bonus Reading: How Can You Make Managing Your Money More Fun?

Budgeting

One of the fundamentals in personal finance is “spending less than you earn.”

Since teenagers don’t usually have full-time jobs and may not earn any money at all, how can we teach them how to manage their spending?

One way is to allow them to make all of their purchases out of a weekly or monthly allowance.

That way, they’re forced to budget for the things they need and want.

You can ask them to pay for clothing, school lunches, car insurance, and gas (If they’re drivers), school supplies, and entertainment money.

They’ll have to decide how much to spend in each financial category.

They’ll also need to make sure they don’t spend too much cash in one category and run out of money for another.

If you feel comfortable, share your budget with your teen. Be sure to go over all of the periodic or hidden expenses also included in the family budget.

You can explain the difference between gross and net pay. Plus, show them how much money comes out of your wages for taxes, health insurance, and retirement saving.

With teens, showing often works better than telling.

So, giving your child space to make his own financial decisions or showing him your budget will be a more powerful teaching tool than hypothetical advice.

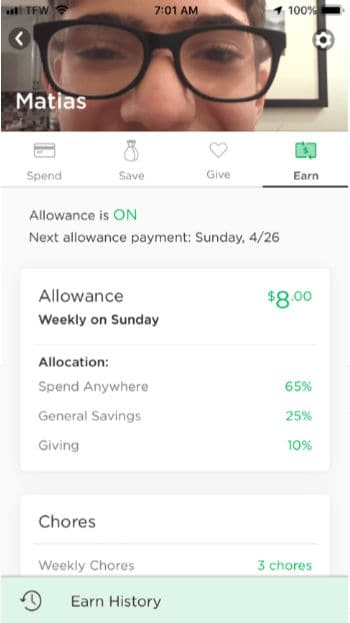

Allowance Cards

How do you give your child her allowance each week? Cash can be a pain to deal with nowadays.

You may consider opening a bank account for your teen and getting her a debit card so you can deposit her allowance directly into her account.

(Note: Most banks require a photo ID, so if your teenager doesn’t have a driver’s license, you may need their birth certificate, Social Security card, or a photo ID from the DMV.)

You can also use services like FamZoo or Greenlight.

FamZoo offers a private online family “banking” system designed to help you teach your kids good money habits.

You, as the “banker,” manage your kids-the “customers” funds through IOU accounts or prepaid cards.

FamZoo will cost you between $2.50 – $5.99 per month for your entire family, depending on whether you subscribe monthly or pay in advance.

Greenlight is a debit-card service for kids that allows you to open a debit card for your children without a bank, as well as monitor their spending and okay spending at specific stores. The service costs $5 per month for up to five children.

How much allowance to give them?

If they’re covering all of their spending, they may need more than the national average (currently $30 per week, according to a poll by the American Institute of CPAs).

You can try a dollar amount that fits your family budget, and if you find it’s too low or too high, then adjust accordingly.

Consider requiring your teen to save and invest a portion of their allowance also, to make those money habits automatic.

Additionally, this can be a great time to remind your teen about setting aside some funds to donate to their favorite causes.

Let Them Fail

Teenagers tend to take bigger risks than adults because the area of the brain that controls self-regulation is still in development.

So is it a wise idea to let them take risks with money?

The key is allowing them to fail with money in a lower-stakes setting so that they can learn how to budget before they have to pay for their own apartment, utilities, and food.

This method allows your teen to make decisions about spending with real-world consequences while still in a safe environment.

It will only work, though, if you’re willing to let your child face the consequences of his spending.

Did he run out of money for gas this week?

Instead of giving him more, let him figure out how else to get to school. Maybe he’ll need to catch a ride with you or ask a friend to come to pick him up.

Resist the urge to fix budgeting problems, and he’ll quickly learn to make his money last rather than repeat the discomfort of running out of money.

Borrowing Money

Credit card companies will likely send your teen information about credit cards as soon as she turns 18.

Companies are all over college campuses, encouraging college students to apply for cards.

If your teenager doesn’t know how to manage credit, though, she could get into some big trouble with a credit card.

Research has shown that teens are more likely to think using their limbic systems and make decisions based on feelings. The same research shows that, unfortunately, those decisions are often faulty.

Plus, your teen has had less experience managing money and thus is more likely to make poor decisions. So a credit card could be a dangerous tool in the hands of your teen.

Since your example is often the most powerful to your child (even if it doesn’t seem like it), talk to your teen about the pros and cons of credit cards and loans.

If you use credit cards, explain the power of paying them off in full each month and using them very carefully.

Explain the interest charges and penalties of not paying off your credit card monthly and how paying your card off every month helps you build good credit.

If you’ve given her a bank account and she’s used to spending with a debit card, then a credit card will be less tempting, especially if she’s made a few budgeting mistakes along the way.

With proper discipline, a credit card can be a useful tool for your college student.

Investing

One of the most abstract personal finance concepts for teenagers is investing.

It can be hard for many teenagers to wrap their minds around the idea that saving money now can benefit them in three or more decades.

As a parent, have honest conversations with your teen about investing. If investing a portion of his income becomes a habit now, then he’ll likely continue to invest as he grows older.

You can show him charts that demonstrate the power of compound interest.

Explain how money invested is at risk but that some risk is necessary.

Encourage him to set up an IRA in his teenage years or set one up for him (see below for more information).

An added benefit to talking about investing is that it helps your child think beyond immediate goals, like saving for a car, and helps them develop longer-term financial planning skills.

The word “millionaire” is powerful to a teenager, so show him how he can become a millionaire by saving small amounts of money early and giving it lots of time to compound.

One example: if your teen saves $5,000 per year, starting at age 18, for ten years ($50,000 total) and allows that money to grow, with an average 7% return, until he’s 65 years old, he’ll have over $1,000,000.

Jobs

There are several advantages to teens having a job.

First, it teaches responsibility and how hard she has to work to earn a dollar. Second, it allows your child to open an IRA with her earnings.

If your child has a W-2 or 1099 job (in other words, earned income that she has to file an income tax report on), she is eligible to save in her IRA. She can save 100% of her earnings, up to $6,000 per year, in an IRA.

As a parent, you can “match” her earnings and put money in on her behalf, up to $6,000 per year, as long as it’s less than any earned income.

You can help your teenager find a traditional job or encourage her entrepreneurial spirit by helping her think through opening a dog-walking or babysitting business.

That income, if reported to the IRS, can allow her to start an IRA as well.

Teaching Teens Financial Topics

Even if you don’t feel 100% confident in your own personal finance skills, start conversations with your teenager about money.

Your child doesn’t expect you to be perfect, and talking through your own money mistakes can be powerful lessons for your child.

Explore using some financial apps to help your kids learn about managing money.

Check out some personal finance books from the library or order from your favorite bookseller. Then read and discuss them together.

The lessons you teach your teenager about money now are laying the groundwork for a lifetime of positive earning, saving, and investing behavior.

Good money habits can set your teen up to become financially independent from you early in life and can change a lifetime of struggling with money into a lifetime of money confidence.

Next: How Can I Help My Teenager Understand Big Loans?

Article written by Laurie

Laurie is a team member of Women Who Money and the founder of The Three Year Experiment, a blog about building wealth in order to become location independent.